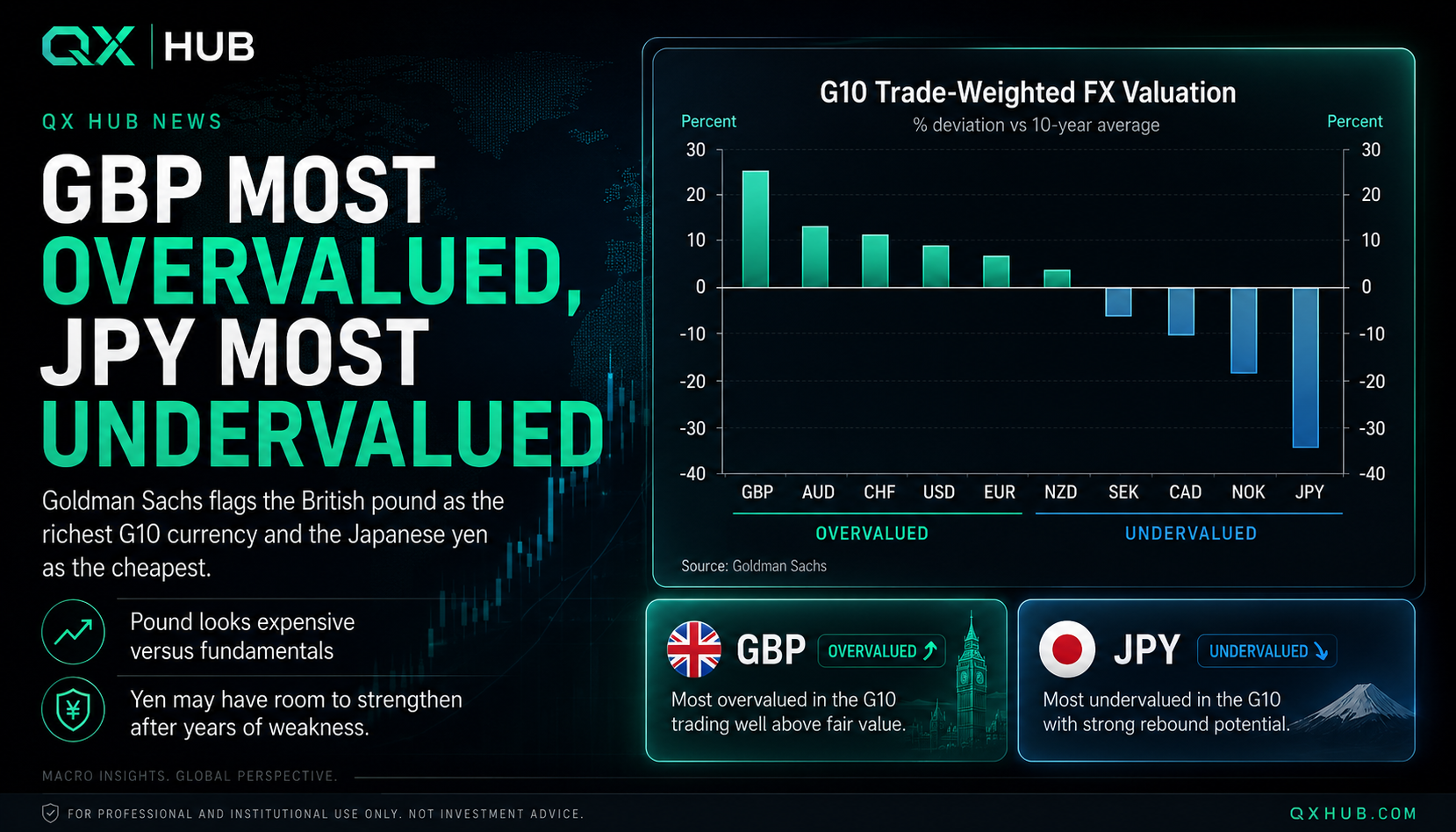

‼️ Goldman Sachs' G10 FX valuation screen puts sterling at the expensive end of the table and the Japanese yen at the deepest discount. In plain trader language: GBP is priced with a lot of good news already inside it, while JPY still carries years of weakness in the chart.

That does not make the pound an automatic short. Valuation is not a trigger by itself. It tells us where the market is paying a premium. If UK inflation, wage data or Bank of England expectations cool, that premium can become fragile faster than a headline suggests.

The yen side is the more interesting pressure point. JPY has been punished by the carry trade, the U.S.-Japan yield gap and slow Bank of Japan normalization. If global yields ease, risk appetite slips or the BoJ sounds firmer, the cheapest G10 currency can reprice sharply.

What to watch now: GBP/JPY for the cleanest valuation clash, USD/JPY for dollar and intervention risk, EUR/GBP for sterling fatigue, plus U.S. yields, DXY, UK CPI, BoE comments and BoJ language. One chart is not enough; the setup needs confirmation.

QX Hub take: treat this as a map, not a button. Expensive currencies can stay expensive in a trend, and cheap currencies can stay cheap while carry pays. The professional move is to mark the imbalance, wait for price confirmation and keep risk small around central-bank headlines.